Journalist

Hassan Shittu

Journalist

Hassan Shittu

Share

South Korea’s central bank has issued a stark warning over the growing risks of won-pegged stablecoins, cautioning that private issuers could threaten monetary stability if safeguards are not established.

The Bank of Korea (BOK) said in a new report titled “Currency in the Digital Age: Harmony of Innovation and Trust” that the rapid expansion of stablecoin activity poses systemic vulnerabilities, including potential depegging events and illicit capital flows.

The central bank’s concerns come at a time when South Korea is actively debating how to regulate stablecoins.

Can South Korea Balance Stablecoin Innovation With Monetary Stability?

The BOK, led by Governor Rhee Chang-yong, reiterated its position that only regulated financial institutions, preferably banks, should issue such assets, arguing that “non-bank issuers could undermine monetary control and capital management.”

The central bank’s latest analysis emphasized that the severity of reserve asset volatility could directly affect the domestic financial market, warning that improper collateral management may lead to depegging risks similar to those seen with foreign dollar-backed stablecoins.

The report highlighted risks to monetary stability from privately issued stablecoins, particularly those that might fail to maintain a one-to-one reserve ratio with the Korean won.

The BOK cautioned that improper reserve management, foreign capital outflows, and speculative trading could trigger a loss of peg confidence, echoing the failures seen in algorithmic stablecoins such as TerraUSD in 2022.

The report shows that stablecoins, while potentially improving payment efficiency and supporting financial innovation, could also undermine the effectiveness of monetary policy and disrupt foreign exchange management.

It called for robust reserve audits, issuance caps, and central oversight to prevent liquidity shocks.

The statement follows months of mounting tension between the BOK and the government.

In June, South Korea’s ruling Democratic Party proposed the Digital Asset Basic Act, which would allow local firms to issue stablecoins with a minimum capital requirement of 500 million won ($367,000) while ensuring full redemption guarantees.

The bill, backed by President Lee Jae-myung’s pro-crypto administration, seeks to increase transparency and competition in the local digital asset market.

However, the Bank of Korea has consistently opposed letting non-bank entities issue won-pegged stablecoins.

At the time, Governor Rhee insisted that any digital currency backed by the won should remain under the central bank’s purview.

“Allowing private companies to issue won-denominated stablecoins without adequate supervision could weaken monetary control,” Rhee said earlier this month.

The Stablecoin Race Is On — and Korea’s Banks Aren’t Waiting.

Despite central bank opposition, commercial banks have been preparing for a gradual rollout.

In June, eight major banks, including KB Kookmin, Shinhan, Woori, and Nonghyup, formed a consortium to develop a joint won-linked stablecoin.

The consortium plans to pilot two issuance models: a trust-based system, where customer deposits are held separately as reserves, and a deposit-linked system, where stablecoins mirror customer deposits on a one-to-one basis.

The banks say the initiative aims to “secure independence and competitiveness” amid fears that foreign dollar-backed stablecoins could dominate the domestic market.

The consortium’s creation marks a shift in South Korea’s financial sector, which has historically maintained distance from digital assets.

Bank executives privately acknowledge a “shared sense of crisis” that foreign dollar-pegged stablecoins could dominate the domestic market if local issuance lags behind.

Meanwhile, the Financial Intelligence Unit (FIU) is restructuring its anti-money laundering (AML) protocols to address the upcoming “institutionalization” of stablecoins.

The agency has commissioned research on risk mitigation and is drafting new AML guidelines for stablecoin issuers to be completed by December.

Officials said the findings will form the foundation for updated oversight rules under the amended Specific Financial Information Act next year.

South Korea’s Stablecoin Bills Stall in Parliament as Agencies Vie for Control

Notably, the government is also tightening coordination across agencies.

While President Lee previously proposed dismantling the Financial Services Commission (FSC), it remains active in crypto oversight and is expected to serve as the main licensing authority for KRW-pegged stablecoins.

Pending bills from both ruling and opposition lawmakers would give the FSC power to approve issuers, enforce redemption standards, and impose emergency orders in case of market disruption.

Political debate has slowed progress, however. Four separate draft bills are stalled in the National Assembly as lawmakers and regulators clash over whether fintech and IT firms should be allowed to issue stablecoins.

The BOK argues that such permission could lead to the emergence of “private currencies” controlled by large tech conglomerates like Naver and Kakao, potentially challenging the central bank’s monetary authority.

Despite the gridlock, the stablecoin sector continues to attract global attention.

In August, Circle CEO Heath Tarbert met with Governor Rhee and executives from major Korean banks and crypto exchanges to discuss cooperation on stablecoin infrastructure and regulatory frameworks.

Also, Solana Foundation partnered with Korean blockchain infrastructure company Wavebridge to build a “compliance-ready” KRW-pegged stablecoin.

The debate unfolds against a backdrop of declining domestic crypto activity.

According to the BOK’s Financial Stability Report, the Korean crypto market lost nearly $24 billion in value in the first half of 2025, with daily trading volumes falling 80% to 3.2 trillion won.

Retail investors have shifted to local equities amid stronger currency performance and growing regulatory uncertainty.

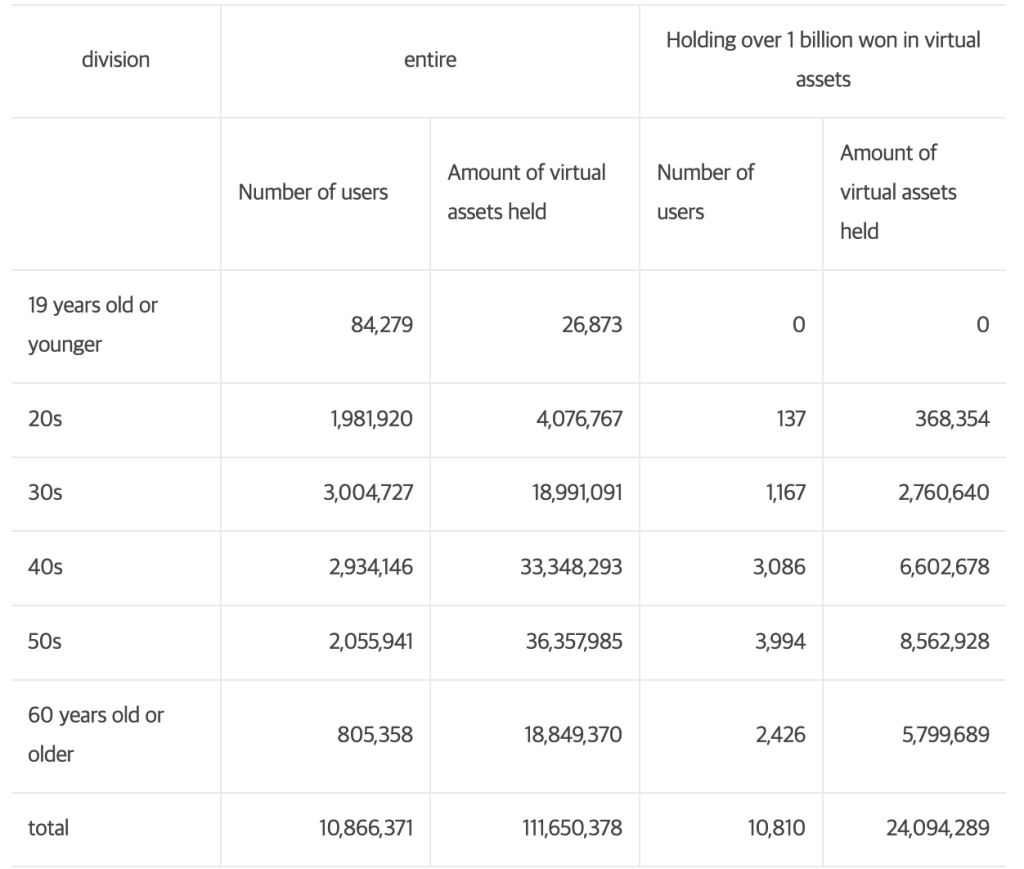

Still, South Korea remains one of the most active crypto markets in Asia, with over 10.8 million trading accounts, roughly 20% of its population.